The more things change, the more they stay the same

Chris Nikolaou, 18 November 2024

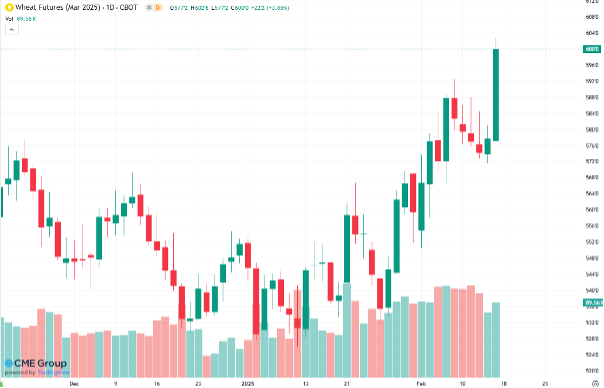

The Advantage programs have concluded for the 2023/24 season with the last of the sales programs completed in October. September saw a rebound in pricing for both domestic and international markets due to dry weather in Australia, Russia, the United States and South America. Over October we saw improvements in many of these global producing regions and a late rain event in the Southeast of Australia was viewed as somewhat positive. The Australian harvest is approximately 30% complete with many growers focused on marketing canola and pulses. Overall, the price outlook is positive for wheat pricing in the new year as the Russian Ag Ministry could be in the process of reducing their export quotas for the second half of their marketing year.

Global weather improves over October into November

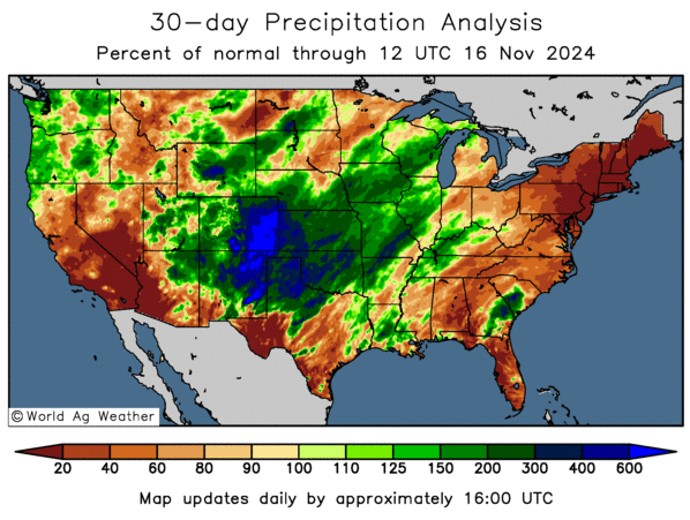

The southern plains of the United States have been battling drought, on and off, for over two years now. However, in late October and early November a pattern change brought much needed rainfall to some of the most parched areas of the wheat belt.

US futures have responded by dropping back to lows not seen since the end of northern hemisphere harvest in August. The South American monsoon was late to arrive this year. This weather pattern usually kicks off late September but did not arrive until mid-October and is now in full form. The market’s fears for Brazilian beans and corn have subdued while the monsoon remains in place.

Australian Update

Most growing regions of Australia experienced an unusually dry September. This exasperated the problem for those hardest hit by this season’s dry in SA and VIC. A mid-October late rain event through the southeast is seen by growers in southern NSW and VIC as beneficial, but unfortunately, too late for growers in SA.

At the date of writing, the national harvest is approximately 30% complete. Oilseeds and pulse harvest is almost complete, with growers starting to switch their focus from harvesting these commodities to marketing them. The northern areas of NSW and WA are coming in slightly better than expected in terms of yield, but the market is waiting for results in the frost and dry affected areas of southern NSW, VIC and SA.

From a marketing perspective, Australia is currently seeing good demand for wheat into Asia. Exporters are reporting active buying from Malaysia, Indonesia, Philippines and Thailand. Also, it has been reported that China was in buying Australian wheat a fortnight ago.

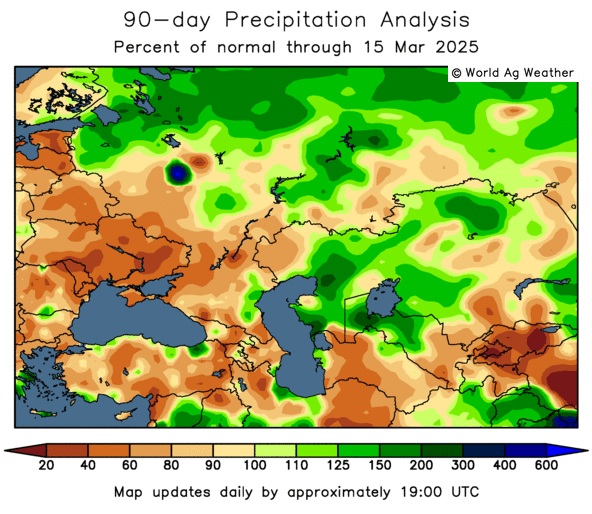

Russian rumours on export quotas for exporters

Russia has experienced a dryer than normal 2024. Initially, this impacted the current season production earlier in the year. Production was reduced by some 9MMT in 2024 vs 2023. Timely rains helped, but the overall pattern has been poor. Over the last few months, locals have sowed their winter wheat program which is currently tracking at approximately a million less hectares from a year ago. There has been talk that the Russian Ag Ministry will seek to restrict exports over Q1 – Q2 of 2025 due to the production and seeding issues they have faced this year. If the current weather pattern stays in place, this will be more likely. Any restrictions set for the first half of the year will be very good for Australian prices as global buyers will also be faced with declining stocks in the EU and Ukraine.

What does it all mean for Australian grain prices?

Global markets have softened as major production areas receive rain after periods of dryness. However, Russia, the world’s largest wheat exporter is still dryer than normal and more likely to restrict exports if this weather pattern stays in place. Australian harvest is now in full effect and over the coming weeks we will better understand the damage caused by frost and dryness. As the title of this article suggests, the more things change, the more they stay the same. Grain market volatility looks set to continue as we continue through the Australian harvest and throughout the next marketing year. Utilising Advantage Grain’s dedicated team to manage your grain sales in a structured, low risk way, will save you time and could yield real pricing benefits in the new year as this expected price volatility plays out across the globe.

Advantage Grain would like to take this opportunity to thank all the growers throughout QLD, NSW, VIC and SA for your support over 2024 and we wish everyone a safe and bountiful harvest. May your yields be off the chart and high quality!

Share This Article

Other articles you may like